Introduction

We all know what it’s like to pay bills each month: rent, utilities, phone, maybe a car, insurance. It feels routine. But what if the line between “normal monthly payments” and a debt trap is thinner than you think? When your monthly payments are a debt trap instead of just bills, that routine becomes something far more dangerous.

In this post, I’ll walk you through how to know when your monthly payments aren’t simply bills but are trapping your finances. We’ll explore the warning signs, compare what bills should look like vs what a debt-trap payment structure often is, and provide a roadmap to escape. The tone will be conversational—because this isn’t just about numbers; it’s about your life, your security, your peace of mind.

What it means when your monthly payments are a debt trap instead of just bills

Let’s clarify the difference between having regular monthly bills (which most of us do) and being caught in a debt trap.

Bills: Regular, predictable payments that you’ve budgeted for (rent, utilities, streaming subscriptions, loan/lease you can afford), which leave you space to save or invest.

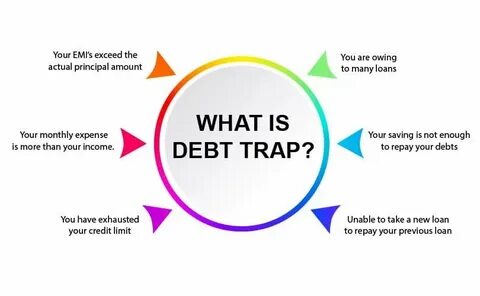

A debt trap: A situation where monthly payments (loans, credit-cards, EMIs, subscriptions, financing deals) are so large, frequent, or high-interest that they leave little to no financial flexibility, force you to borrow or rollover debt to meet obligations, and grow over time. One financial resource defined a debt trap as “when repayments become more than you can manage” with mounting interest and a shrinking buffer. (Pocketly)

When payments are a debt trap instead of just bills, you might find yourself:

- Paying for past-choice (e.g., large purchases) rather than present-freedom.

- Covering recurring payments that leave you little room to save or respond to emergencies.

- Using new credit to pay existing obligations.

- Feeling trapped rather than in control.

A recent article lists key warning signs you’re falling into a debt trap: borrowing for everyday essentials, credit card balances increasing, avoiding looking at bills, being stuck in a borrowing cycle. (Achieve)

Powerful Steps: First-Time Job Salary in the US — What You Must Set Aside Before It’s Too Late 1.

Why you might be paying bills that are actually a debt trap

How does this happen? Why do what look like “just monthly payments” evolve into a debt trap? Here are several reasons:

- High interest debt: You may think you’re paying a monthly “loan” but if the interest is huge, the balance may barely shrink.

- Excessive proportion of income: When monthly payments consume a large share of your take-home, you have less flexibility for life’s surprises.

- Recurring commitments you barely use: Lots of subscriptions, leased items, or “buy now, pay later” arrangements that you forget about, but still commit to payments.

- Rolling over debt: Using new loans/credit cards to pay older ones — a classic debt-trap mechanism.

- Lack of emergency buffer: Without a buffer, any shock forces you to take on debt, increasing payments.

- Automatic upgrades/leasing: New car leases, latest gadgets, high monthly payments disguised as “minimal monthly cost”.

- Financial instability: If income fluctuates, you may struggle to cover those monthly commitments reliably.

A study of debt trap dynamics found that convenience (installment plans, easy credit) and consumer behaviour (materialism) play a strong role in making payments become a trap. (sciencedirect.com)

Signs Your Monthly Payments Are a Debt Trap Instead of Just Bills

Here are clear warning signs you should watch. If you recognise several, your monthly payments may have crossed from manageable bills to a debt trap.

- You’re only making minimum payments on credit cards or loans. (Hoyes, Michalos & Associates Inc.)

- A large portion of your income goes directly to fixed monthly commitments, leaving little to save.

- You borrow or use credit to cover essential costs (e.g., groceries, utilities).

- You feel anxious or stressed when bills arrive or payments post.

- You rely on new credit to pay old credit (balance transfers, new loan to pay debt).

- You can’t adjust your budget much—cutting one payment affects the rest of your life.

- You have many small monthly payments (subscriptions, leases, financing deals) you don’t actively monitor.

Table: Comparison – Healthy Monthly Bills vs Debt Trap Monthly Payments

Here’s a table to illustrate the difference in a more concrete way:

| Feature | Healthy Monthly Bills | Debt Trap Monthly Payments |

|---|---|---|

| Proportion of income | Payments take a manageable portion (e.g., ≤30-40%) | Payments take large portion (e.g., 50-70% or more) |

| Flexibility | Enough left to save and buffer | Little to no room for saving or surprises |

| Use of credit | Minimal or well-managed | Heavy reliance on credit or new borrowing |

| Payment growth | Stable or decreasing over time | Balance or payments growing over time |

| Financial stress | Predictable and manageable | Frequent worry, stress, sleepless nights |

| Buffer/emergency fund | Some savings exist | No buffer, one shock away from crisis |

Use this table as a diagnostic tool: if your monthly payments align more with the right column than the left, you’re likely in a debt-trap zone.

The Real Cost of Treating Monthly Payments as a Debt Trap Instead of Just Bills

Why does it matter so much? Because when payments become a trap, your future gets compromised:

- Less ability to save or invest: Every dollar tied up in high payments is a dollar not building your future wealth.

- Higher cost of borrowing: When you rely on credit more, you may face higher interest rates or worse terms.

- Reduced financial resilience: Without buffer, you’re more vulnerable to job loss, health crises, or unexpected expenses.

- Lifestyle limitation: With payments dominating income, you may feel stuck in a job you don’t enjoy because you must pay.

- Mental/physical health impact: Debt stress has been linked to poorer health outcomes and higher anxiety. (RSIS International)

- Long-term compounding of negative effect: It’s not just one bad payment—trap payments build cumulative load.

When monthly payments transition from being “manageable bills” to “debt trap obligations”, you’re effectively paying not for a service or asset you enjoy, but for a previous decision or financing structure that drags you backward.

How to break free: Turning your monthly payments back into just bills (not a trap)

Here’s a practical roadmap to help you shift from debt trap payments toward manageable bills and financial freedom.

Step 1: Get a full picture

- List all your monthly payments: rent/mortgage, utilities, subscriptions, car loan/lease, credit-cards, EMIs.

- Identify which payments you can control or reduce (subscriptions, non-essential leases).

- Calculate what percentage of your take-home pay goes to these payments.

Step 2: Categorise payments: healthy vs trap-risk

Ask yourself for each payment:

- Does it provide value today (you use it, benefit from it)?

- Is it affordable in different income scenarios (e.g., if your income falls 20%)?

- Does the balance or payment amount tend to increase?

If the answer is “no” or “uncertain”, flag it for adjustment.

Step 3: Target high-risk payments first

Focus on payments that:

- Carry high interest (credit cards, sub-prime loans)

- Are large relative to your income

- Are recurring but you rarely use (unused subscriptions, leases)

- Require you to borrow to pay them

Step 4: Reduce, restructure, eliminate

- Cancel or pause subscriptions you rarely use.

- Downsize or negotiate your lease or loan.

- Refinance high interest debt or consolidate payments (carefully).

- Automate minimum payments and schedule additional debt payments.

- Move surplus toward the highest cost payments first—debt avalanche or snowball methods apply.

Step 5: Build breathing room

- Create an emergency fund so you don’t rely on credit when a shock hits.

- Create a “buffer account” (e.g., one month’s expenses) to ensure you aren’t living paycheck to paycheck.

- After pressing payments are under control, allocate saved amounts to savings and investing.

Step 6: Monitor and adjust regularly

- Monthly review: Are payments still manageable? Are some sliding toward risk again?

- Quarterly scan: Has your income changed? Have your obligations scaled up?

- Make sure your payment-to-income ratio remains healthy (e.g., payments <40-50% of take-home pay depending on context).

By doing this, you convert your payment obligations from a trap into manageable bills that support your lifestyle—not imprison it.

Real-Life Example: When Monthly Payments Became a Debt Trap—and How Recovery Looked

Meet Jasmine. She had a steady job, an apartment in a city and a car lease. Over time she added many subscriptions—streaming, fitness, premium apps—and used a credit-card to cover extra expenses. Her monthly payments summed up to about 60% of her take-home pay, leaving little for savings or emergencies. When her car required unexpected repair and her lease payment rose, she took out a high-interest personal loan. The payments snowballed.

She realised her monthly payments were not just bills anymore—they were a trap. She took these steps:

- Reviewed every monthly payment, cancelled unused services.

- Ended her car lease early and opted for public transport + cheaper car.

- Transferred loan into debt consolidation with lower interest.

- Built a small emergency fund to avoid future borrowing.

Within 12 months, her monthly payments dropped to 35% of income. She went from reacting to crises to managing proactively. Her story illustrates the shift: monthly payments as a trap vs monthly payments as support.

Why this matters: Beyond the numbers

When your monthly payments trap you, it’s not only about money—it’s about freedom, choices and lifestyle. Two things happen:

- You stop living for tomorrow’s potential: Every paycheck serves yesterday’s decisions instead of today’s options.

- You lose agency: You feel bound by payment commitments rather than empowered by savings and flexibility.

Turning monthly payments from a debt trap into just manageable bills is about reclaiming your agency, your freedom, and your ability to direct your life rather than being constrained by it.

Final Thoughts

If you’ve sensed your monthly payments are more exhausting than empowering—take this as your nudge: when your monthly payments are a debt trap instead of just bills is when your financial future needs a reset. The sooner you act, the sooner you regain control.

Here’s your action list:

- This week: list all monthly payments and calculate what % of income they represent.

- Flag any payment that seems large, growing, or providing little value.

- Next week: pick one high-risk payment and reduce or eliminate it (subscription, refinance, downgrade).

- Within 90 days: reduce payments to a sustainable level (e.g., <40-50% of take-home).

- Ongoing: build buffer and emergency fund so future shocks don’t become new traps.

Your monthly payments should support your life — not control it. When you see them as just bills you can manage, you open up space for saving, growing, exploring and yes—living. It’s not about being debt-free immediately; it’s about being debt-smart, free to choose how you live rather than how your payments live you.

Start today. Because turning payment-traps into manageable bills is one of the best moves you can make for your financial future.